Agentic Commerce

The acceptance layer for agent-driven purchases — complete a checkout at any merchant, integrated or not, with the cardholder's consent and credential.

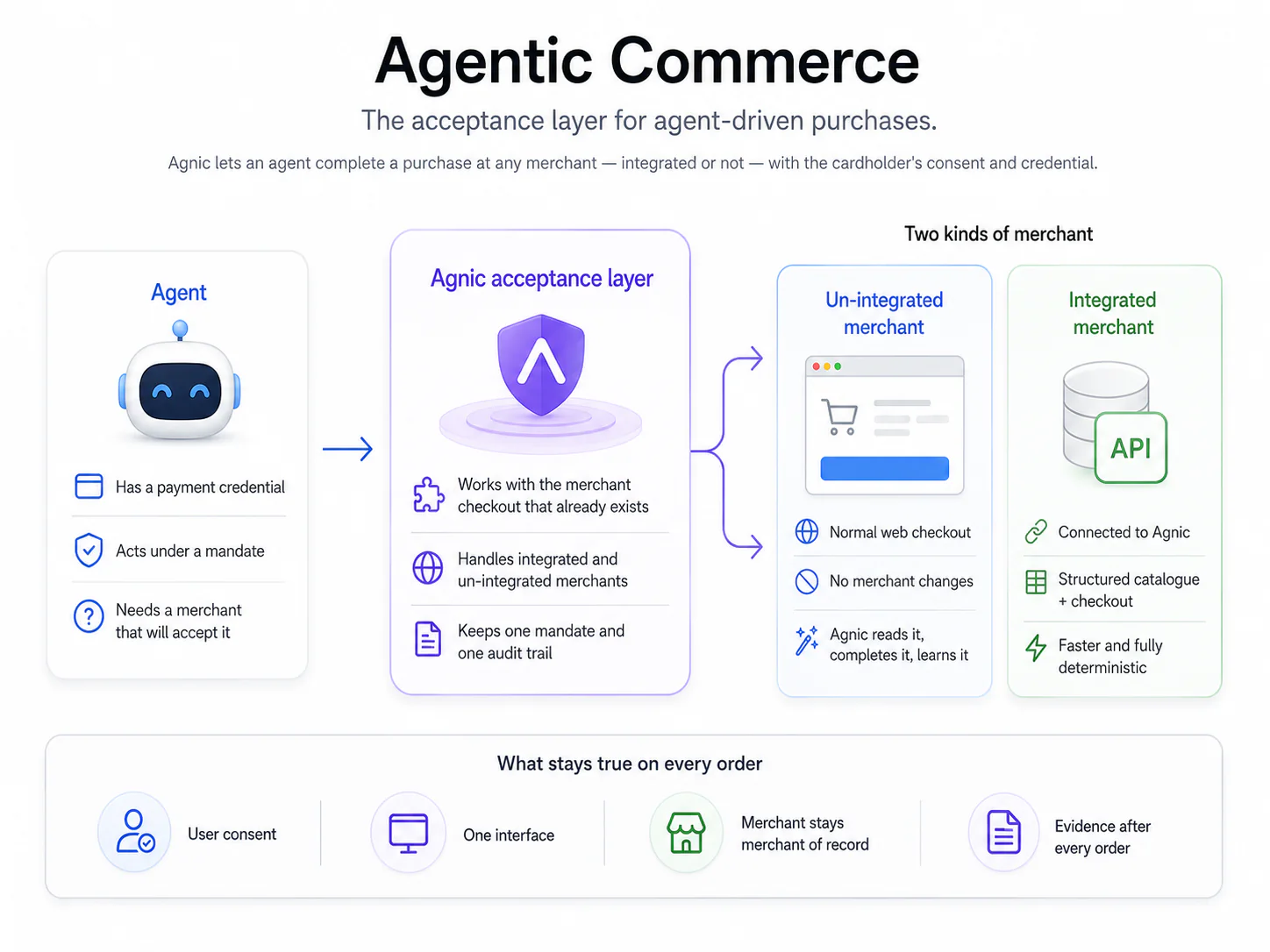

Agentic Commerce

Issuers and networks can now give an AI agent a payment credential of its own — a Visa Intelligent Commerce network token, a Mastercard Agent Pay token, a passkey-bound cryptogram scoped to a single mandate. Authorising the agent to pay is no longer the hard part. Finding a merchant that will take the payment is.

Agnic is the acceptance layer. The Agnic Checkout Engine completes a merchant's existing checkout on the agent's behalf — the same checkout a person uses — so an agent's credential is accepted at a merchant that was never built to take one. One integration for the issuer; the whole merchant internet for the cardholder.

This documentation is open to everyone. Production checkout execution is available to approved partners — contact Agnic for access. The interface is the Agnic MCP server and REST API.

Two kinds of merchant

Every merchant an agent meets is in one of two states. Agnic handles both — through one interface, under one mandate, with one audit trail.

Un-integrated merchants

No agent checkout — just an ordinary web checkout. The Agnic Checkout Engine reads it, completes it, and learns it. This is most of the internet. Start here.

Integrated merchants

Connected to Agnic — a structured catalogue and a server-to-server checkout. Faster, richer, fully deterministic.

| Un-integrated | Integrated | |

|---|---|---|

| Merchant work | None — its checkout is unchanged | Connects a catalogue + checkout endpoint |

| How Agnic orders | Completes the live checkout | Server-to-server session |

| Coverage | The long tail — most merchants | Merchants on the Agnic network |

| Fulfilment | As the checkout offers | Structured options (pickup, delivery, fees) |

Most of the value is the first column: the merchants that will never integrate. Completing their checkout — reliably, repeatably, at a success rate you can report — is the hard problem, and the one an issuer's credential runs into first. See Un-integrated merchants.

What funds the purchase

Agnic is credential-agnostic. Today it completes checkouts with a PCI-vaulted card: the agent and the model operate on a non-sensitive alias, and the real number is substituted inside the vault as the request leaves — it never touches the agent, the model, or the page.

The same engine is built to carry issuer-provisioned agentic credentials — including Visa Intelligent Commerce network tokens, minted from a mandate-bound intent — so the credential an issuer gives its agent is what completes the purchase at the merchant. Explore and Pay are the same either way.

How an order works

Two calls: Explore, read-only, which prices the order and returns a one-use confirmation token, then Pay, which executes only against that token and the user's explicit confirmation.

Explore never charges; Pay charges exactly the amount its token was issued for. To see it end to end on a real checkout, read the bakery walkthrough.

Common questions

Who is the merchant of record? The merchant. Every order is charged by the merchant through its own payment processor. Agnic never holds or moves funds.

Does the model ever see the card? No. The agent and the model operate on a non-sensitive alias; the real number exists only inside a PCI-DSS-scoped vault, where it is substituted into the payment request in flight.

What stops a runaway agent? The mandate. Spending limits and identity grants are enforced server-side on every order; anything outside them stops for an explicit passkey approval.

What does a merchant have to change? Nothing. The Agnic Checkout Engine completes the merchant's existing checkout. Merchants that want a structured rail can connect to the network.

What exists after an order? A verifiable record: the user's instruction, their confirmation, the exact amount approved, the claims disclosed, and step-by-step evidence of the checkout itself.